From 2017 to 2023, the compound annual growth rate of low-power wide area network connections will reach 109%. By 2023, the total number of connections will exceed 1.1 billion, and users will spend more than US$4.7 billion on such connections. NB-IoT and LoRa have accounted for 70% of the market share, and this proportion will continue to grow, reaching 85% in the next 5 years.

Recently, the well-known German Internet of Things research company IoT Analytics released the latest report "LPWAN Market Report 2018-2023" to conduct detailed research and analysis on the low-power wide area network (LPWAN) market. Beginning in 2018, low-power wide-area networks have become a key driving force for the growth of IoT connections. By 2023, the number of LPWAN connections will exceed 1.1 billion. However, this scale is only less than 10% of the total number of Internet of Things connections.

With a compound growth rate exceeding 100%, NB-IoT and LoRa will become market oligarchs

As we all know, LPWAN technology provides low power consumption and low data rate communication in a wide area. On a global scale, whether it is the release of public networks or the deployment of private networks, it is in a trend of rapid development. Driven by network deployment and suppliers, the number of connections based on low-power wide area networks will also achieve rapid growth. IoT AnalyTIcs predicts that between 2017 and 2023, the compound growth rate of low-power wide area network connections will reach 109%. The total number of low-power wide-area network connections in 2023 will exceed 1.1 billion, and users will spend more than $4.7 billion on such connections. Due to the high degree of market fragmentation, NB-IoT, LoRa, and Sigfox will become mainstream LPWAN technologies, no matter from the application status of end users or from the perspective of industrial ecology. However, it is expected that NB-IoT and LoRa will occupy the vast majority of public and private networks respectively.

2017-2023 growth in the number of LPWAN connections

IoT AnalyTIcs pointed out that the above data comes from in-depth research on global low-power wide-area network deployment and 9 industry application companies. In fact, IoT AnalyTIcs conducts comparative research from multiple perspectives: from the perspective of technology categories, the low-power wide area network is divided into Sigfox, LoRa, NB-IoT, LTE-M, and other five categories for comparative research; from the perspective of dependent spectrum , Respectively inspected authorized spectrum and unlicensed spectrum; from the perspective of network deployment methods, respectively investigated two methods of public network and private network; from the perspective of application, respectively investigated smart agriculture and forestry, smart buildings, smart health, home & consumption, industrial Customers in 9 industries including Internet of Things, Retail, and Smart City.

IoT AnalyTIcs analysts believe that the current low-power wide area network market is still in its infancy, and this stage is characterized by a high degree of technological fragmentation. However, market concentration will quickly form. LoRa has been in a leading position for the past two years. However, NB-IoT will develop faster due to the support of mainstream operators around the world, and may surpass LoRa in the leading position by the end of 2018. Judging from the current market, NB-IoT and LoRa have accounted for 70% of the market share, and this proportion will continue to grow, reaching 85% in the next 5 years.

Of course, as a large-scale market, demand differentiation in various industries is the norm. Coupled with the long-tail market's preference for non-mainstream technologies, low-power wide-area networks cannot form an absolute monopoly. NB-IoT and LoRa will occupy 85% of the market in the future, and the remaining less than 15% of the market will be realized by other low-power wide-area network technologies or similar complementary technologies. At present, there are more than 20 similar technologies providing services in the field of Internet of Things. Although the number of connections is very limited, most of them are still implemented in some niche markets.

Various LPWAN and related technologies

In 2023, there are 1.1 billion LPWAN connections and 4.7 billion US dollars in connection expenditure. The average revenue per connection is only more than 4 US dollars, and this continuous decline in average revenue is a high probability event. From this perspective, if IoT network operators only provide connection services, their revenue ceiling is very obvious.

Diversified connection methods, LPWAN only accounts for a small share

Although low-power wide area networks will achieve a growth rate of more than 100% in the next few years and become a key factor in new connections, more IoT devices are still connected through personal area networks and local area networks, and according to Choose a variety of connection methods for various scenarios. IoT Analytics predicts the proportion and growth of various connections in the Internet of Things in the future. The relevant data is shown in the following figure:

The growth rate of various connection methods of the Internet of Things

It can be seen from the above data graph that low-power wide-area networks only account for less than 8% of the Internet of Things connections, and occupy the third position in the market share of Internet of Things connection methods. The Internet of Things has diversified connection methods. According to the classification of IoT Analytics, various connection methods of the Internet of Things include:

Wireless Personal Networks (WirelessPersonal Networks, WPAN)

It can be seen that the wireless personal area network (WPAN) is the most commonly used connection method among all Internet of Things devices, and this type of connection method generally does not exceed a range of 100 meters at most. Such devices include devices connected by Bluetooth, such as headsets; also devices connected through Zigbee and Z-wave in smart homes, such as smoke alarms, thermostats, etc. In addition, IEEE also recommends high-frequency 802.15.3 (TG3, also known as UWB).

Wireless Local Area Networks (WirelessLocal Area Networks, WLAN)

The second largest share of the number of connections is wireless LAN devices, which can generally reach distances of hundreds of meters. Among them, WiFi is the most typical technology in this field, running on unlicensed 2.4GHz and 5GHz. WiFi devices are also experiencing rapid growth and are commonly found in household appliances, smart TVs, and smart speakers. However, WiFi connections are also used in some industrial IoT scenarios, such as factories, and will still play a key role in the future.

Low-power Wide Area Networks (LPWAN)

The fastest growing IoT connection in the next few years will be low-power wide-area networks. By 2025, it is estimated that nearly 2 billion devices will be connected through low-power wide-area networks. This technology is to ensure long battery life and long coverage (up to 20 kilometers). At present, the mainstream technologies that have formed are Sigfox, LoRa and NB-IoT. Dozens of countries around the world have deployed networks supporting these three types of technologies. More than 25 million devices are connected through these technologies. Of course, the most important devices are still Smart meter.

Wired connection

When we talk about the Internet of Things, few people take wired connections into consideration. However, in many scenarios, wired connection is the most reliable way. Especially in some industrial scenarios, both fieldbus and industrial Ethernet use wired connections. In the future industrial IoT scenarios, wired connection will still be a major issue. Connection method.

Cellular M2M

2G/3G/4G technology has been the only choice for wide-area, mobile IoT device connection for a long time. With the commercialization of low-power wide-area networks and 5G, it is expected that the share of IoT connections through these traditional cellular communication technologies will decline.

5G

5G is very inclusive. Although 5G has not yet been commercialized, various propaganda has made it one of the core technologies to accelerate the era of the Internet of Things, but more of the driving force is led by the government or government-related forces, especially in China. In the United States, the first 5G network will provide fixed wireless access (FWA) services for residents and small and medium-sized enterprises at the end of this year. More use cases will not appear until all 5G standards are frozen in 2020.

Wireless Neighborhood Area Networks (WirelessNeighborhood Area Networks, WNAN)

In terms of distance, the wireless neighborhood network is between the wireless local area network and the wide area network. Typical representatives of this technology include Mesh networks, such as Wi-Sun, JupiterMesh, and so on. In some scenarios, this technology will be used as an alternative to LPWAN or cellular networks (such as utility field networks), and in some scenarios, this technology is a supplement to LPWAN or cellular networks, such as indoor The depth of meter reading covers blindness. As the LPWAN-related technology family listed in the previous article, some of them belong to WNAN.

other

Other Internet of Things communication technologies, including satellite communications and some inconvenient and specifically unclassified network technologies, although the number is very small, will also play an irreplaceable role in the field of Internet of Things in the future.

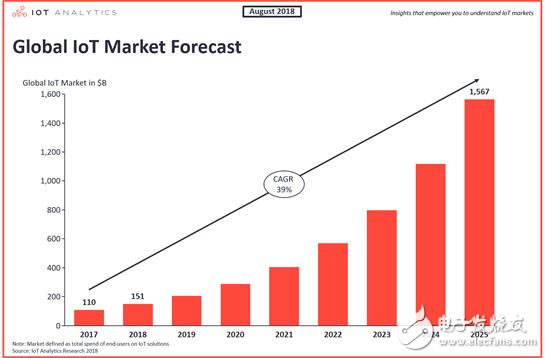

IoT market size

For the research on the market size of the Internet of Things, IoT Analytics uses the end user's expenditure on the Internet of Things solution as an indicator of the market size. In the past 2017, the global Internet of Things market was about 110 billion U.S. dollars, in 2018 it was about 151 billion U.S. dollars, and it is expected to reach 1.56 trillion U.S. dollars by 2025, with a compound annual growth rate of about 39%. In 2023, LPWAN connection expenditure is only 4.7 billion US dollars, which is less than 1% of the total market size of the Internet of Things, which once again illustrates the ceiling of LPWAN connection costs.

Taking the end-user's expenditure on IoT solutions as the market scale, it can be regarded as calculated by the expenditure method. From this point of view, the output value of the IoT is still 6 years away from the trillion-dollar market scale. As the main force in the development of the Internet of Things industry, China will account for the highest proportion of the global Internet of Things output value in the future. Assuming that this proportion is 25%, according to the forecast of the IoT Analytics market size, it is expected that after 2022, China’s Internet of Things Only the scale of the industry can exceed RMB 1 trillion.

The bimetal thermometer combines two metals with different linear expansion coefficients, and one end is fixed. When the temperature changes, the two metals have different thermal expansion, which drives the pointer to deflect to indicate the temperature.

WSS series bimetal thermometer is a kind of field measuring instrument for measuring medium and low temperature. It can directly measure the temperature of liquid, steam and gas medium in the range of - 80 ℃~+500 ℃ in various production processes. It is suitable for temperature measurement when the precision is not high in industry. As a temperature sensing element, bimetallic sheet can also be used for automatic temperature control.

The bimetallic thermometer can be divided into axial, radial, 135 ° and universal types according to the connection direction of the pointer plate of the bimetallic thermometer and the protective tube.

â‘ Axial bimetal thermometer: the pointer plate is vertically connected with the protective tube.

â‘¡ Radial bimetal thermometer: the pointer plate is connected with the protective tube in parallel.

③ 135 ° directional bimetal thermometer: the pointer plate is connected with the protective tube at 135 °.

â‘£ Universal bimetal thermometer: the connecting angle between the pointer plate and the protective tube can be adjusted at will.

Bimetal Thermometer,Explosion Proof Thermometers,Pointer Bimetal Thermometer,Boiler Pipes Pointer Thermometer

Henan New Electric Power Co.,Ltd. , https://www.newelectricpower.com