In fact, under the keyword "failed privatization", rapid Internet searches have led to a long list of global failures, from Europe, to Africa, the United States, South America and Asia. This Columbia University paper and Michael Hudson's paper "Let Us Get Glory in Inequality" are worth reading.

Privatization of state-owned assets or solemn operational services and functions are a simple choice for the government to raise funds to contribute to its budget. Privatization can effectively improve the efficiency of the management of some assets or services-when these assets or services are subject to free market forces and competition, there is privatization instead of state monopolies and privileged rents to obtain private monopoly, which is to protect against free market competition. In practice, the state transfers the privilege of using public assets or services to obtain rents to wealthy private investors. This is the disadvantage of privatization, especially in so-called "natural monopolies", or when there is no alternative, the public is forced to use key strategic assets or services. For example, there are toll roads, water, general sanitation services, power grids, or prisons.

Dissatisfaction with this privatization model has prompted many countries to call for a reversal of this situation.

In another interesting research paper, author Mildred E. Warner emphasized "the reason why the privatization experiments in the 1980s and 1990s failed to materialize. But this reverse privatization process is not a return to the old model. On the contrary, it heralds the emergence of a new balanced position, which combines the use of the market, careful consideration and planning to reach the best possible decisions that are both efficient and social.†Then suddenly, I suddenly realized that what I did was It is-instinctively and out of anger after the Genoa incident-is exactly what we need to achieve this new "more balanced position".

Therefore, I restarted the original proposal and wrote this article, which expands the use of blockchain and token economics as a viable model to reverse the errors and dysfunctions of the strategic public sector Privatization.

I would also like to thank my colleagues Thomas Euler and Karl Michael for providing me with valuable feedback and ideas on the management of this new model.

Due to the rapid development of the cryptocurrency field, I hope to see new developments and innovative methods to solve this problem frequently. Therefore, I think this model is very "popular" and will be subject to future revisions and improvements.

Use token economics

Although the origin of the tokenized economy can be traced back to the early 19th century, the term now usually borrows cryptocurrency to refer to the widespread use of an economic incentive system to positively influence the behavior of stakeholders´ behavior model. "Token Economics" is a branch of social research. It is no different from traditional economics, except that it pays close attention to behavioral economics and game theory in order to provide correct economic incentives to promote individual behavior.

Create a blockchain-based system to manage public assets

The following template can be applied to a strategy of public assets or serving society as a whole, but ideally, the state always retains control of at least such assets in order to protect society from abuse of power by private operators. For example, these assets are vital water sources and their supply infrastructure, energy plants and power grids, public roads, minimum medical services and infrastructure, and prisons.

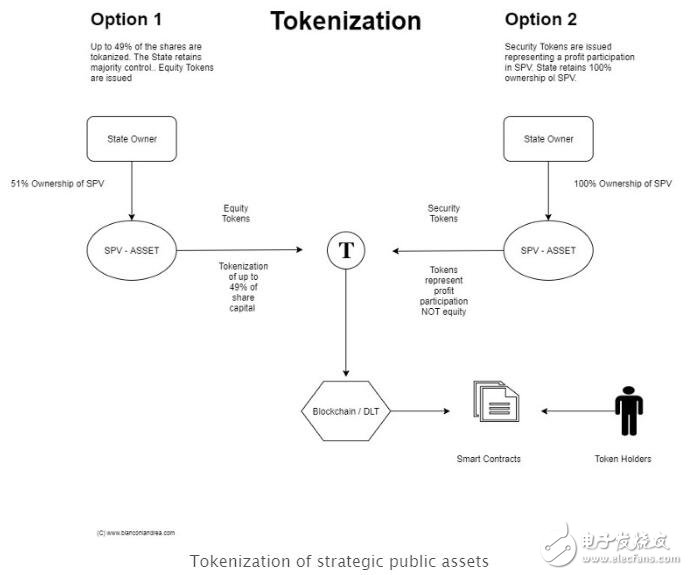

1. Tokenization: equity or security tokens

The term "tokenization" is mainly related to securities, stocks and physical assets. It indicates the creation of a digital token, which represents different types of rights-such as ownership, some economic payments, voting, and so on. This token is usually issued on the blockchain.

In the proposed model, it can be easily distributed to stakeholders and smart contract terms, and it can be added to ensure that certain provisions are automatically implemented with the key to the incentive mechanism.

Strategic public assets will be transferred to a special purpose vehicle ("SPV"). There are two options here.

· Option 1 is to mark SPV shares by issuing stock tokens, and combine ownership, voting rights, and profit distribution rights through smart contracts.

· Option 2 is to issue security tokens, which does not represent the participation of SPV equity, but only the economic right to share the profits of SPV.

The difference between these two options is: (1) Issuance of stock tokens in Option 1, correspondingly transfers the corresponding ownership of the SPV; (2) The applicable company law will stipulate the voting rights of shareholders, and thereby all Token holders of shares exercise voting rights. This may reduce the flexibility of governance. In addition, since the applicable company law also stipulates procedures for transferring shares (such as company registration and notary public), these "real world" settlement procedures are very complicated, which affects flexibility and intelligent automation of the execution of contract terms. Therefore, I came to the conclusion that the second option is better, because: A) SPV is always 100% in the hands of the public; B) The security token issued does not represent the equity in the SPV, but only the payment currency C) Even though this is still a guarantee for the application and compliance of securities laws, the issuer has almost no restrictions when designing related monetary rights and their role in governance. D) Issuance is not restricted by physical ownership, such as Option 1 (1 share 1 token) or calculated by the value of the shares, only based on the profitability of SPV-A. If it is not enough, the country is willing to take measures to make up for the shortfall; E) Such security tokens can also be airdropped to key stakeholders. In short, option 2 seems to be much more flexible.

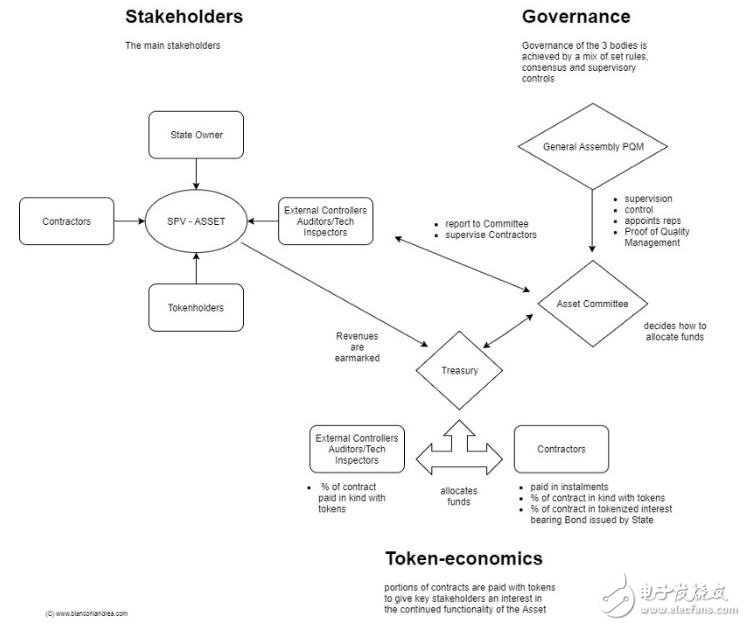

2. Main stakeholders and capital flows

The main stakeholders will be:

The country that owns the assets;

· Citizens who use public services/assets;

· Maintenance and service contractors;

· Token holders.

The flow of funds will be:

· Fees collected by SPV, such as public road tolls or utility fees;

·SPV maintenance services and repair costs.

3. Blockchain and DLT

In my first proposal, I advocated the use of open-access public blockchains.

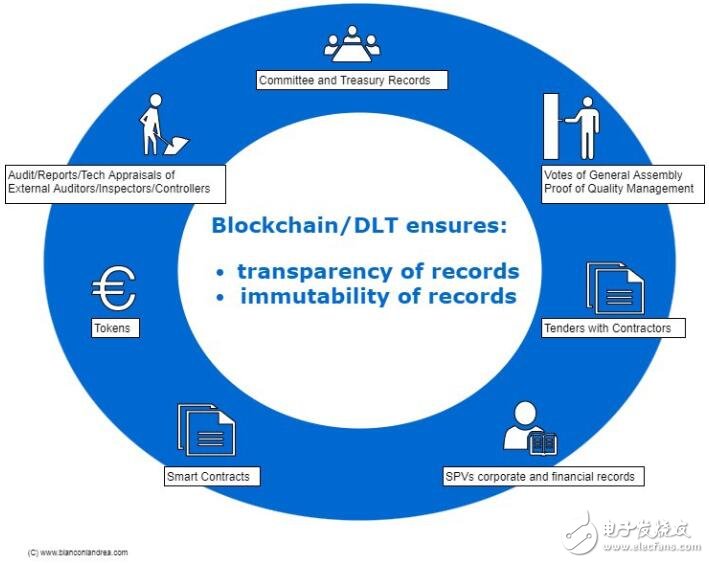

Some commentators also questioned the necessity of blockchain in this model. There has been some confusion surrounding the term "blockchain". This term is now widely used to refer to any type of DLT, of course not only the first and purest blockchain, the Bitcoin protocol. Therefore, using blockchain DLT in this model actually means creating an asset accounting system that stores records. Since the construction of DLT is modular and optional, there is no need to build a completely permissionless and decentralized blockchain like Bitcoin. Some functions can be decentralized, while others can be centralized. In addition, to ensure more decentralized supervision and control, centralization can still be positively affected by governance provisions. In addition, no matter what type of blockchain and consensus protocol are used to make this model work, this is still a technical problem that is beyond the purpose of this article and will be solved by skilled people other than me. It should be noted here that it should mainly ensure (i) transparency and (ii) the immutability of stored records. This means that stakeholders should be able to access all documents such as-SPV's financial shares, maintenance costs, safety reports, engineering reports, public tender procedures, bills from contractors, etc. Everything should be open to the public in the sun. This is a well-known problem. When such a dramatic event happened in Genoa, the key evidence and documents suddenly disappeared from the server.

Blockchain is used to mark public strategic assets

4. Token economics and the right incentives for stakeholders

A balanced system of economic incentives and governance tools is essential to positively influence the behavior of key stakeholders, such as contractors, auditors, and the state itself. The contractor is an important part of it. Especially in public procurement, such as public roads, the poor conditions of public roads and the subsequent maintenance conditions are issues that all citizens are very concerned about. In the best case, this is both the inability of the state to manage resources and a sign that the contractor is responsible for the bad work done. In the worst case, this is a sign of corruption.

In order for contractors to take responsibility, they must have a financial interest in the normal operation and proper maintenance of the income-generating assets. This can be achieved by ensuring that the contractor "has a skin in the game."

In addition to the installment payment when the milestone is reached, the contractor will also use SPV-issued tokens as a payment method. This ensures that the contractor is interested in the continued function of the asset. In the event of a dispute, the public administration will have additional recourse against the tokens allocated to the contractor, which can automatically recover money through smart contract terms.

More "skins in the game" can also be achieved by requiring contractors to subscribe to interested government bonds as a percentage of the contract value. Such government bonds can also be "tokenized" to ensure that if the contractor breaches contractual obligations or the warranty period, the contractor has additional recourse. In a smart custody, this bond will be used as collateral. The flexibility achieved by programming different features in the numeric keys is another key advantage.

5. Governance tools

Adjusting the incentives of private contractors is only part of the game, while influencing the behavior of the state is much more difficult. To do this, we must create the right set of governance tools. The main issue here is to prevent the state from wasting funds and to ensure that it effectively distributes the income generated by the assets. Therefore, in this model, an appropriate set of governance rules for SPV and all stakeholders is essential.

The first step should be to designate the revenue generated by SPV as (i) for maintenance (ii) reinvestment in new infrastructure, and (iii) distribution to token holders. In smart contracts, the proportion of remaining profit redistribution can also be planned in different ways to maximize the incentive mechanism. For example, through rewards, a higher percentage, the most diligent contractor.

The second step is to establish a governance structure

In this model, I conceived three governing bodies, namely, the Ministry of Finance, the Assets Committee, and the General Assembly.

The Ministry of Finance receives income from the SPV, and according to its authorization, distributes the income according to the income shown above, and it distributes the funds in accordance with the instructions of the Assets Committee.

·The Assets Committee is composed of national representatives, token holders and technically qualified professionals in specific industries. The Asset Committee decides how to use SPV’s revenue, based on a set of priorities and reports on asset conditions obtained from third-party controllers, auditors, and technical experts.

·The General Assembly is composed of all stakeholders. It will vote on the composition of the Assets Committee and supervise the allocation of funds made by the Assets Committee after the fact.

Interestingly, my colleague Karl Michael Henneking introduced the concept of Proof of Quality Management ("PQM"), which is basically an evaluation mechanism used to evaluate the efficiency of asset committees in allocating funds. In essence, it is possible to create a rating index reflecting the condition of assets by comparing the satisfaction expressed by its users with the reports of auditors and technical experts. Simply put, the more the fund invests and the less feedback it receives from stakeholders, the lower the rating and therefore the lower the performance of the asset committee. The reverse is also true. The lower the investment amount, the higher the feedback report received, and the higher the asset committee’s rating and performance.

Public strategic asset tokenization governance plan

in conclusion

Although the limitations and functional obstacles of privatization in the past are now obvious and increasingly questioned by the public, the need for new methods and new models of key public strategic asset management has become more and more urgent. The first suggestion I received aroused my interest and surprised me. I also received some inquiries from the public administration, including those from Nigeria on whether this model can be used to reverse the privatization of its power grid. , I hope that blockchain and smart contracts will help create this new model. I hope to see that this model can be applied everywhere, and needs to be managed on the basis of economic and effective public strategic assets, without letting them blindly fall into the hands of private individuals, nor let them fall into the hands of wasteful public.

Now, a new and more balanced strategic public asset and service management model is coming.

Pet Velcro Braided Sleeve,Pet Braided Sleeving,Pet Expandable Braided Sleeving,Cable Protection Sleeve

Shenzhen Huiyunhai Tech.Co., Ltd. , https://www.cablesleevefactory.com